Why I Walk Away From Deals That “Almost” Work

Why I Walk Away From Deals That “Almost” Work

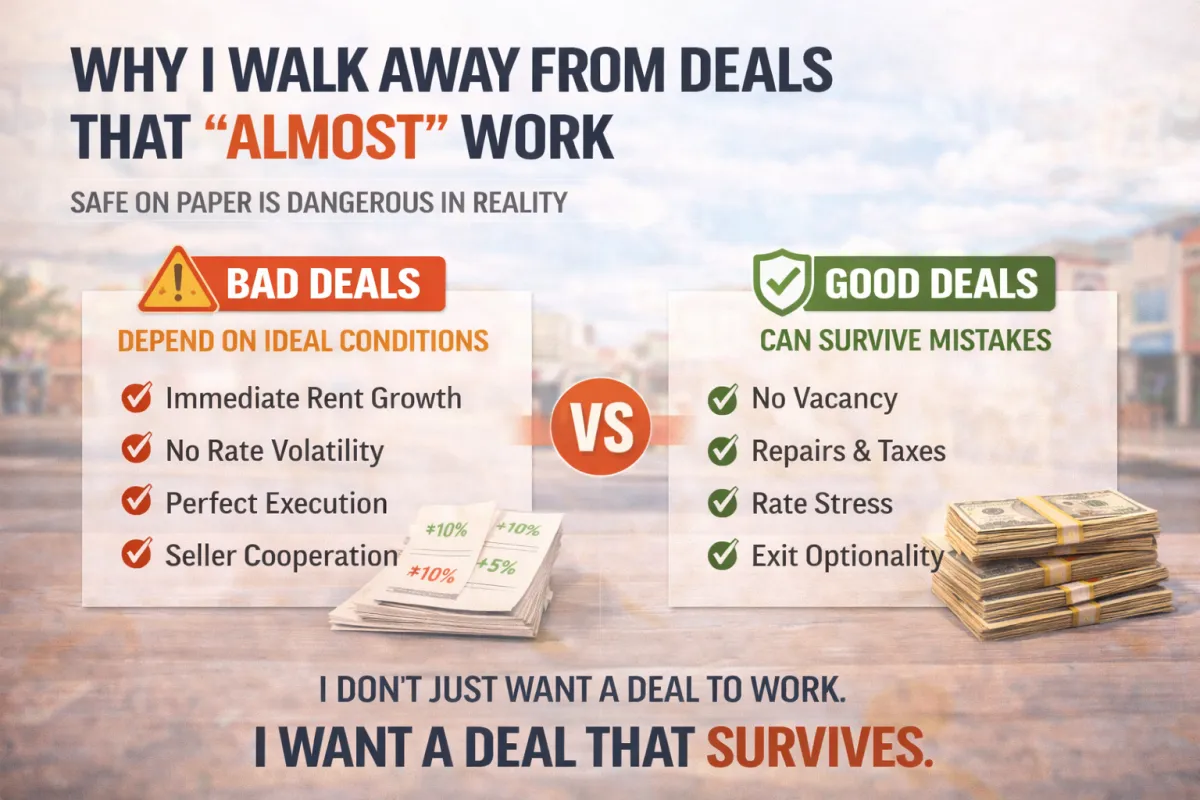

Most bad deals don’t look bad.

They look close.

They pencil if:

Rents grow immediately

Rates cooperate

Execution is perfect

Nothing unexpected happens

Those are the deals I walk away from.

Not because they can’t work —

but because they only work under ideal conditions.

Good deals work conservatively.

Great deals survive mistakes.

Let me show you what I mean using a real deal I reviewed recently.

The “Almost” Deal: Mixed-Use Property in Greenville, SC

This was a mixed-use asset:

Small commercial tenant (tire shop)

Two residential units

Total purchase price: $600,000

On paper, it looked workable.

Not exciting.

Not obviously broken.

Just… tight.

The In-Place Numbers

Gross rents: ~$3,820/month

True NOI after real taxes, insurance, repairs: ~$2,058/month

Property taxes alone were over $15,000/year before appeal

This immediately told me one thing:

The NOI ceiling was low.

Low ceilings change everything.

Where the Deal “Almost” Worked

With standard financing, the deal failed immediately.

So the structure shifted to creative financing:

50% DSCR loan

Seller carry absorbing the remaining balance

Seller carry required to be:

0% interest

No monthly payments

Balloon in the future

Under that exact structure:

DSCR payment ≈ NOI

Cash flow ≈ breakeven

Deal technically “worked”

That’s the danger zone.

Because now the deal required everything to go right.

The Hidden Fragility

Here’s what had to happen for the deal to survive:

No vacancy

No major repairs

No insurance increases

No rate volatility at refi

Seller remaining cooperative long-term

And the biggest risk:

👉 The deal only worked because seller payments were deferred.

That’s not solving the problem.

That’s postponing it.

Why I Don’t Chase “Almost” Deals

This deal didn’t fail because it was stupid.

It failed because it was fragile.

If:

Cash flow disappears with a small expense

DSCR collapses with a minor rate change

The exit only works after perfect rent growth

You’re not buying an asset.

You’re buying a story.

And future lenders don’t underwrite stories.

They underwrite:

In-place NOI

Proven margins

Durable cash flow

The Difference Between Risk and Fragility

Risk is unavoidable.

Fragility is optional.

A risky deal:

Has margin

Has time

Has multiple exits

A fragile deal:

Has one path

Requires precision

Punishes small mistakes

The White Horse Rd deal didn’t fail because it was mixed-use.

It failed because:

NOI had no cushion

Structure absorbed all margin

Exit depended on future cooperation

That’s an “almost” deal.

I pass on those every time.

The Standard I Use Instead

Before I move forward, I want to know:

Does this deal survive flat rents?

Does it survive higher insurance?

Does it survive rate stress?

Does it survive execution mistakes?

If the answer is no — I don’t negotiate harder.

I walk.

Final Thought

Most investors don’t lose money on bad deals.

They lose money on deals that were almost good.

If your deal:

Needs rate relief

Requires immediate NOI growth

Breaks under small stress

It’s not conservative.

It’s optimistic.

And optimism is not a risk strategy.

Want Help Pressure-Testing Your Deal?

This is exactly the work I do with clients.

If you have a deal that:

“Almost” works

Needs creative structure

Depends on a refinance or seller cooperation

I help you:

Stress-test the capital stack

Engineer real exits

Decide whether to fix it or kill it

You can see how I work here:

👉 https://chadchoquette.com/how-i-work

Or review my deal structuring services here:

👉 https://chadchoquette.com/deal-structure-services

Walking away from the wrong deal is a skill.

I can help you build it.