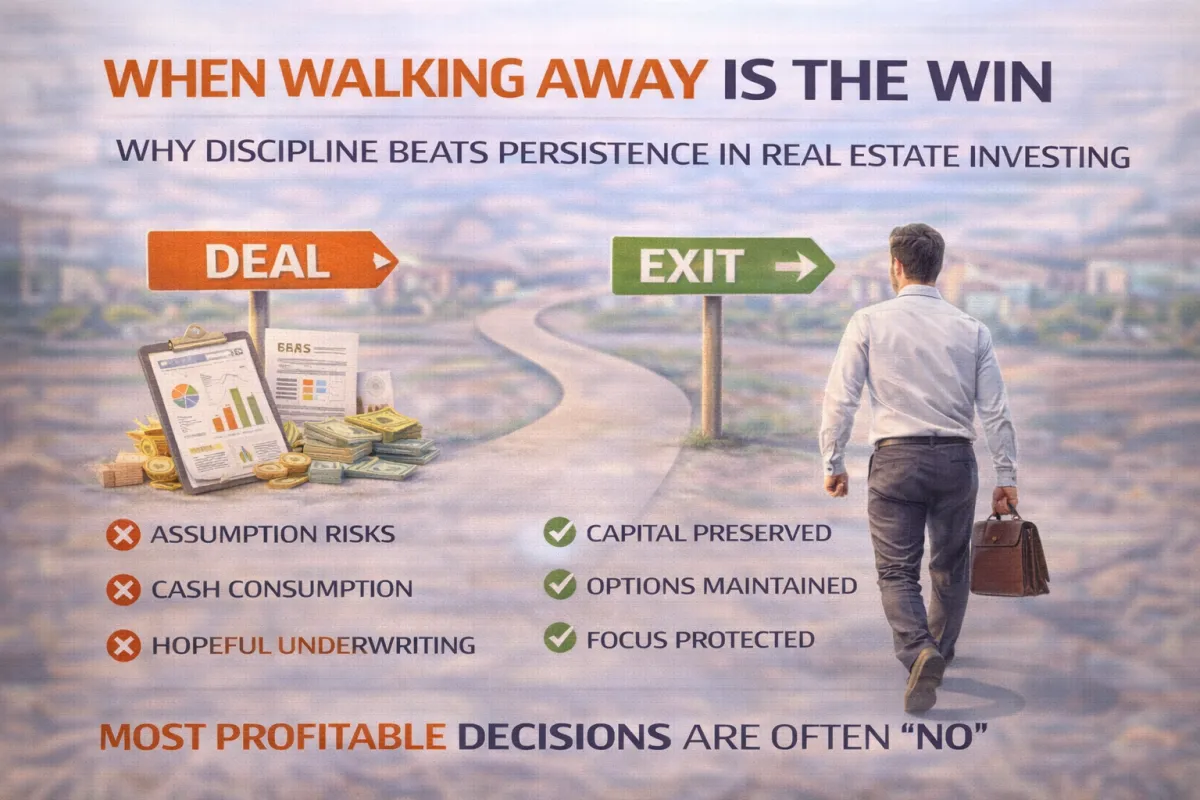

When Walking Away Is the Win

When Walking Away Is the Win

Why Discipline Beats Persistence in Real Estate Investing

Most investors think the win is closing the deal.

In reality, some of the most profitable decisions I’ve ever made came from not closing.

Walking away doesn’t feel like winning — especially after you’ve spent time underwriting, reviewing financials, hopping on calls, and imagining the upside. But sunk cost bias is one of the most expensive traps in real estate.

Bad deals don’t usually announce themselves loudly.

They whisper: “You’ve already come this far.”

This article breaks down why walking away is often the highest-return decision you can make, using a real deal I fully underwrote — and ultimately killed — despite significant time and effort invested.

The Psychology That Destroys Returns: Sunk Cost Bias

Sunk cost bias happens when past effort influences future decisions — even when the numbers no longer work.

In real estate, it sounds like:

“We’ve already spent weeks on this.”

“The seller’s counting on us.”

“We can fix it after closing.”

“We’ll make it work.”

That’s not discipline.

That’s emotional accounting.

Markets don’t care how much time you’ve spent.

Lenders don’t care how hard you worked.

Returns don’t reward persistence — they reward correct decisions.

The Deal That Looked Busy — But Was Broken

North Side Marina & RV Resort — Chico, TX

This was a marina + RV resort deal that initially looked compelling on the surface.

Here’s what the structure required before we even talked upside:

$800,000 seller cash requirement

$300,000 wholesaler fee

~$470,000 assumable SBA loan @ 3.75%

Total cash at close: ~$1.1M

Total implied basis: ~$1.57M–$1.6M

At that point, the question wasn’t “Is there upside?”

It was:

Does the existing business even support this basis?

What the Real Financials Said (Not the Deck)

2024 Actuals (Full Year)

Total Income: ~$462K

Operating Expenses: ~$394K

NOI: –$56,993

True Net Income: –$90,807

This wasn’t a “value-add” problem.

This was a losing business.

2025 YTD (Jan–Sept)

NOI improving, but still modest

Run-rate NOI projected at $45K–$55K/year

Even at a 10% cap, that supports a value of roughly $450K–$550K — not a $1.6M basis.

The Moment Most Investors Make the Wrong Call

This is where deals usually die — or investors double down.

The common rationalizations:

“The assumable SBA loan is cheap.”

“We’ll fix payroll.”

“The restaurant can be optimized.”

“Expansion upside will save it.”

But here’s the truth:

Assumptions don’t erase negative NOI.

And worse — this deal required:

Massive upfront cash

No margin for error

Operational turnaround before safety

A wholesaler fee that consumed real equity

That’s not investing.

That’s hoping.

Why Walking Away Was the Only Winning Move

We walked.

Even after:

Full underwriting

P&L reconciliation

Time spent modeling turnaround scenarios

Conversations with stakeholders

Why?

Because:

The cash requirement was unsupported

The downside was immediate

The upside was speculative

The structure rewarded everyone except the buyer

Walking away preserved:

Capital

Focus

Optionality

Credibility with future lenders and partners

That’s a win.

Discipline Is a Skill — Not a Personality Trait

Good investors don’t close more deals.

They:

Kill bad ones faster

Protect downside relentlessly

Refuse to underwrite “future perfection”

Treat walking away as a decision, not a failure

If a deal:

Requires massive upfront cash

Depends on operational miracles

Justifies price with future fixes

Punishes hesitation

…it’s not “almost working.”

It’s broken.

Where Structure Changes the Answer (And Where It Doesn’t)

Some deals can be saved with better structure:

Seller financing

Deferred payments

Hybrid control structures

Phased acquisitions

Others cannot.

Part of my work is knowing the difference.

That’s why I focus less on “getting deals done” and more on engineering survivable capital stacks.

How I Help Investors Avoid These Mistakes

Most bad deals don’t fail because of price.

They fail because:

Structure is misunderstood

Risk is misallocated

Exit assumptions are untested

If you’re evaluating a deal that almost works, I help investors:

Rebuild the capital stack from scratch

Stress-test refi and exit paths

Identify hidden failure points early

Decide whether to restructure — or walk

You can see how I work here:

👉 https://chadchoquette.com/how-i-work

And review my deal structuring services here:

👉 https://chadchoquette.com/deal-structure-services

Sometimes the most profitable move isn’t buying.

It’s not losing.