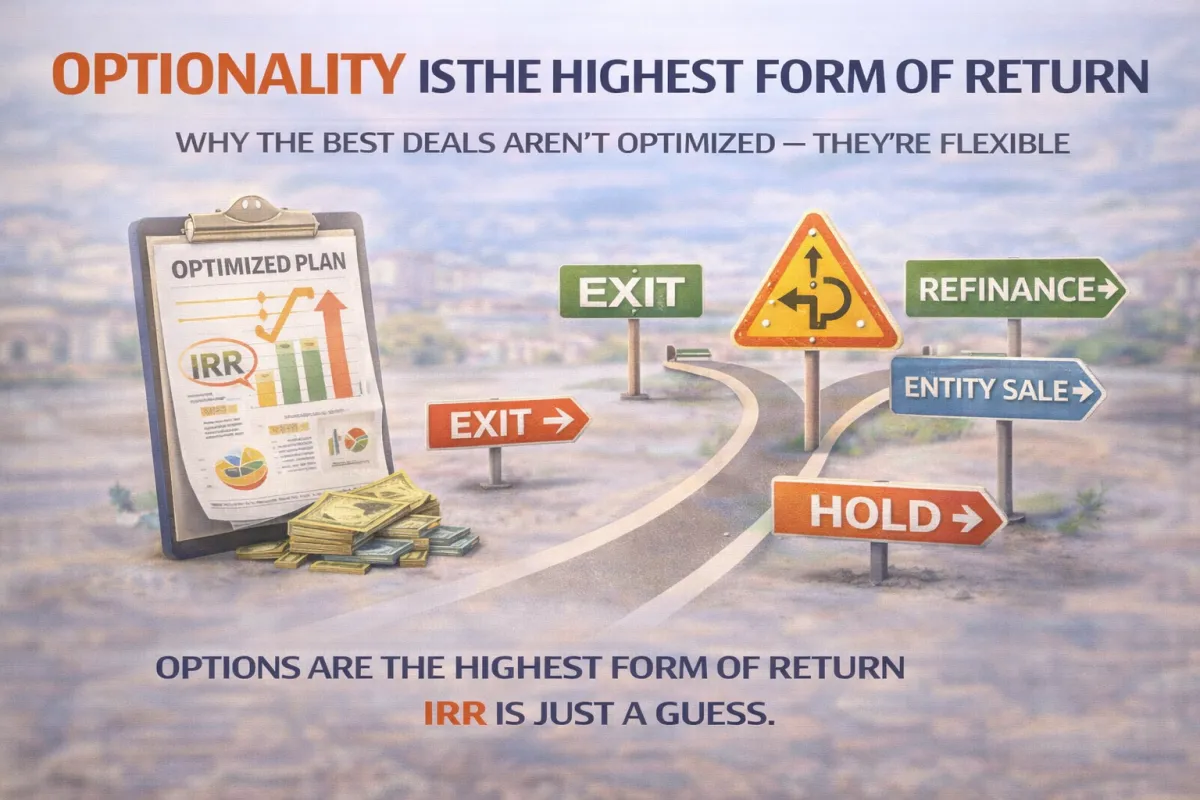

Optionality Is the Highest Form of Return

Optionality Is the Highest Form of Return

Why the Best Deals Aren’t Optimized — They’re Flexible

Most investors obsess over IRR.

Spreadsheets get optimized.

Exit years get tightened.

Returns get modeled to the second decimal place.

And then reality shows up.

Rates move.

Lenders change terms.

Capital markets tighten.

Buyers disappear.

The deal didn’t fail because the IRR was wrong.

It failed because there was no optionality.

The best deals I’ve ever done weren’t the ones with the prettiest pro formas.

They were the ones that gave me choices.

Choices on when to exit.

Choices on how to exit.

Choices on who the buyer could be.

Optionality is the highest form of return — because it keeps you alive when the spreadsheet breaks.

Let me show you what I mean with a real deal.

The Problem With “Optimized” Deals

Most deals are engineered for one outcome:

• One refinance

• One exit window

• One buyer profile

• One capital market assumption

That’s not a strategy.

That’s a bet.

When everything works, these deals look brilliant.

When one assumption breaks, they collapse fast.

Optionality is what allows you to survive imperfect execution — and still win.

Case Study: 708 E Main St — Why This Deal Worked Because of Optionality

This property was acquired using a creative finance stack, not because it was flashy, but because it created flexibility.

The Capital Stack (Simplified)

• Subject-to senior mortgage

• Large subordinate seller note at 0%

• No aggressive refinance assumptions baked in

• No dependency on immediate NOI growth

On paper, it didn’t look “optimized.”

In practice, it gave me multiple exits.

The Exit Paths That Existed From Day One

1. Traditional Refinance

If rates normalized and NOI supported it, a refinance could retire the seller note and improve cash flow.

That was one option — not the only one.

2. Entity Sale Instead of Asset Sale

Because the deal was structured cleanly at the entity level, I could sell the LLC membership interest instead of the real estate.

That unlocked:

• Full depreciation basis transfer to the buyer

• Assumed debt counting toward basis

• No loan disruption

• No forced payoff of underlying notes

This exit worked even without a refinance.

3. Hold With Asymmetric Cash Flow

With low or deferred seller payments, the deal could simply be held while waiting for a better capital environment.

Time was on my side — not the lender’s.

Why Optionality Beats IRR

An IRR spreadsheet assumes:

• One exit date

• One valuation method

• One buyer

• One capital market

Optionality assumes:

• Markets change

• Buyers behave differently

• Capital tightens and loosens

• Execution is never perfect

The deals that survive are the ones that don’t need perfection.

They have room to breathe.

What Optionality Actually Looks Like in Deal Structuring

Optionality is created by structure, not optimism.

It shows up as:

• Seller financing that buys time, not just cheap money

• Capital stacks that don’t force refis

• Exit paths that include entity sales, not just dispositions

• Deals that still work if rates stay higher longer

If your deal only works when one thing happens, it’s fragile.

If it works when several things happen — or don’t — it’s durable.

This Is How I Structure Deals for Clients

When I help investors structure deals, the goal is not to maximize returns on paper.

The goal is to:

• Preserve flexibility

• Reduce forced decisions

• Create multiple exits

• Engineer survival first, upside second

That’s exactly how I approach deals inside my Deal Structure Services.

If you’re buying:

• Creative finance deals

• DSCR-dependent assets

• Mixed-use or business-backed real estate

• Or anything with refinance or balloon risk

Then optionality should be the first thing you underwrite — not the last.

You can learn how I work here:

👉 https://chadchoquette.com/how-i-work

And if you want help structuring or stress-testing a deal for real-world risk, not spreadsheet comfort:

👉 https://chadchoquette.com/deal-structure-services

Final Thought

IRR looks great in hindsight.

Optionality keeps you alive long enough to get there.

The best deals don’t force you into one future.

They give you choices.

And in uncertain markets, choices are the real return.