Seller Motivation Does Not Equal Seller Flexibility

Seller Motivation Does Not Equal Seller Flexibility

One of the most common mistakes I see investors make is assuming that a motivated seller will automatically agree to good terms.

They won’t.

Motivation and flexibility are not the same thing.

And only one of them pays the bills.

A seller can be emotionally exhausted, burned out, or desperate to exit — and still refuse to structure a deal that actually works.

If you don’t separate why a seller wants out from what they are willing to do, you’ll waste time, money, and energy chasing deals that can never close safely.

Let me show you exactly how this shows up in real underwriting.

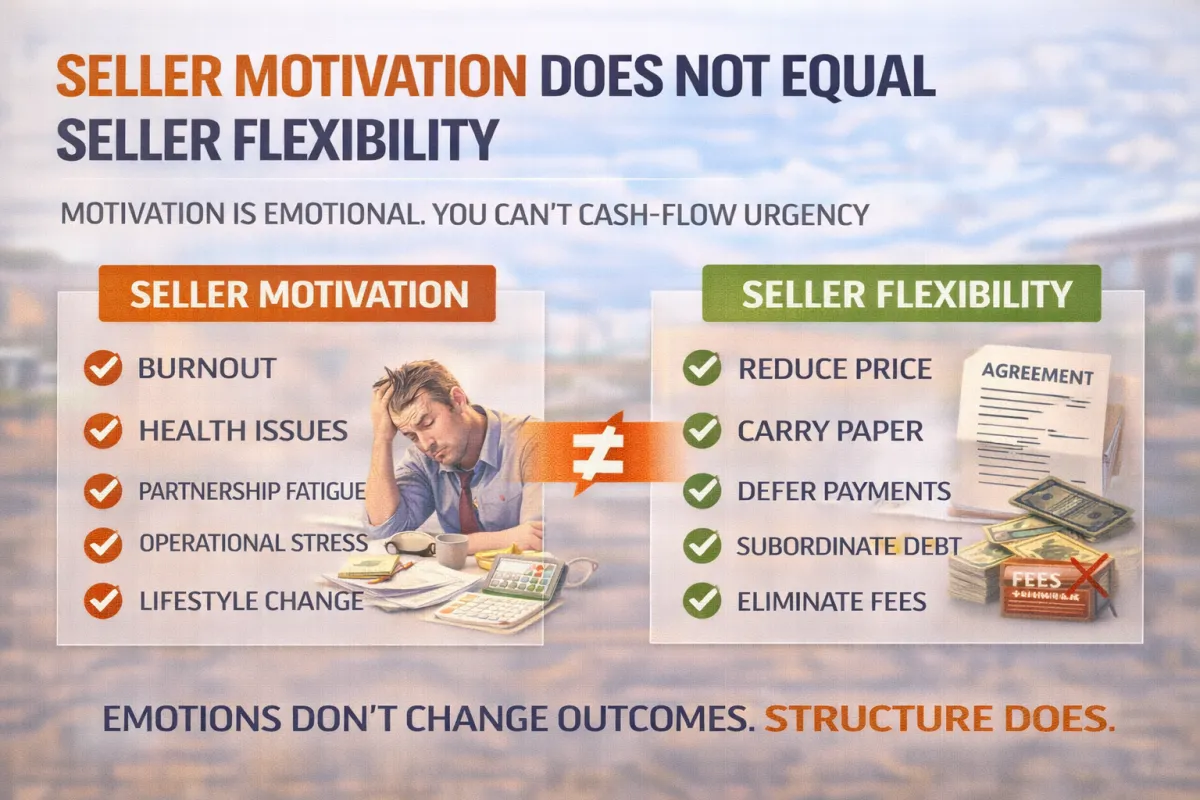

Motivation Is Emotional

Flexibility Is Structural

Seller motivation is emotional:

Burnout

Health issues

Partnership fatigue

Operational stress

Lifestyle change

Seller flexibility is structural:

Willingness to reduce price

Willingness to carry paper

Willingness to defer payments

Willingness to subordinate debt

Willingness to eliminate fees or friction

Only structure changes outcomes.

You can’t cash flow motivation.

You can’t pay a mortgage with urgency.

You can’t refinance “I’m tired.”

Case Study: North Side Marina & RV Resort (Chico, TX)

This deal is a textbook example of high motivation with zero flexibility.

The Seller Story (Very Motivated)

On the surface, the seller narrative was compelling:

Tired of operating a complex marina + RV resort

Restaurant and bar draining time and energy

Open to walking away from day-to-day involvement

Willing to sell and “move on”

This felt like a motivated seller.

But structure told a very different story.

The Structural Reality (Not Flexible)

Here’s what the deal actually required:

$800,000 seller cash at closing

$300,000 wholesaler fee paid upfront

Existing SBA loan ≈ $470,000

Total cash required ≈ $1.1M

Total implied basis ≈ $1.57M–$1.6M

That alone should raise red flags.

But then we underwrote the real numbers.

The Numbers Killed the Deal — Not the Seller

2024 Actual Performance

Total Income: ~$462K

Total Operating Expenses: ~$394K

NOI: –$57K (negative)

Net Income: –$90K

2025 YTD (Better, But Still Weak)

Projected NOI run-rate: ~$45K–$55K

Even under optimistic assumptions, the entire business supported a value closer to $500K–$600K, not $1.6M.

So what was the seller actually motivated to do?

👉 Exit emotionally

👉 But not move structurally

They wanted:

Full liquidity

Wholesale markup preserved

No real price reset

No meaningful seller financing

That’s not flexibility.

That’s a liquidation fantasy.

Why This Deal Had to Be Killed

This deal only becomes viable if:

The $300K wholesale fee disappears

The seller carries a large portion of the price

Cash in is dramatically reduced

Basis resets to reflect real NOI

None of that was on the table.

So despite clear motivation, the deal had no structural path to safety.

Walking away wasn’t pessimism — it was discipline.

The Investor Mistake This Exposes

Most investors hear:

“The seller is motivated”

And they translate it to:

“The deal will work”

That’s a fatal leap.

Here’s the correct framework:

Motivation tells you a conversation is possible

Flexibility determines whether a deal is viable

Structure determines whether you survive ownership

If a seller won’t move on:

Price

Paper

Payments

Or timing

Then motivation is irrelevant.

How I Underwrite Seller Flexibility (Not Just Motivation)

When I review deals, I look for specific structural signals, not stories:

Will the seller carry meaningful balance?

Will payments be deferred or interest-only?

Is price flexible relative to NOI?

Are fees adjustable?

Can risk be redistributed?

If the answer is “no” across the board, the deal is already dead — even if the seller is exhausted.

Final Thought

Motivated sellers are everywhere.

Flexible sellers are rare.

Your job as an investor isn’t to empathize with motivation — it’s to engineer survivable structures.

If the structure doesn’t change:

Cash flow doesn’t change

Risk doesn’t change

Outcomes don’t change

And no amount of seller urgency will fix that.

How I Help With This (Soft CTA)

This is exactly what I do in my deal structuring work.

I help investors:

Separate seller emotion from economic reality

Identify whether flexibility actually exists

Engineer capital stacks that survive imperfect execution

Kill bad deals before they drain capital

If you’re reviewing a deal and aren’t sure whether the seller is truly flexible — or just motivated — that’s a conversation worth having.

You can see how I work here:

👉 https://chadchoquette.com/how-i-work

And the deal structuring services I offer here:

👉 https://chadchoquette.com/deal-structure-services

Because motivation doesn’t pay the mortgage — structure does.