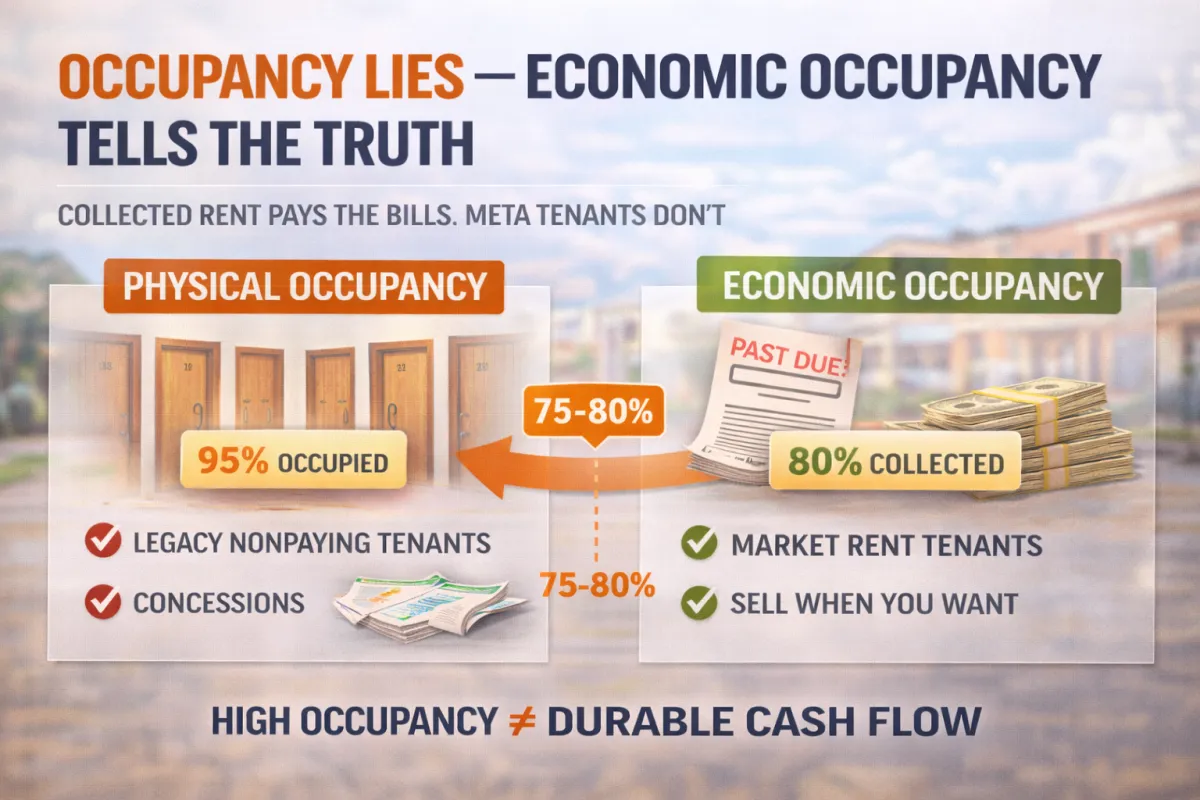

Occupancy Lies — Economic Occupancy Tells the Truth

Occupancy Lies — Economic Occupancy Tells the Truth

One of the most dangerous phrases in real estate underwriting is:

“It’s 90% occupied.”

That statement sounds comforting.

It feels safe.

It feels like demand is proven.

But physical occupancy does not pay the bills.

Economic occupancy does.

I’ve walked away from multiple deals that looked “full” on paper but were quietly bleeding cash once you looked under the hood. This article breaks down why high occupancy can be misleading, how to spot the warning signs early, and how one real portfolio nearly fooled buyers who didn’t dig deeper.

Physical Occupancy vs. Economic Occupancy (Quick Definition)

Physical occupancy = units that are filled

Economic occupancy = rent actually collected at market-supported levels

You can have:

95% physical occupancy

75–80% economic occupancy

And that gap is where deals break.

The Real Deal: Summer Park Portfolio — Killeen, TX (95 Units)

This was a 95-unit workforce housing portfolio spread across three nearby properties in Killeen, Texas.

At first glance, it looked solid.

What the Broker Marketed

~90%+ occupancy

“Stabilized” multifamily portfolio

Value-add upside

Seller financing available

Recent CapEx spend

To many buyers, that checks all the boxes.

But here’s what actually mattered.

What the Occupancy Didn’t Tell You

1. Legacy Tenants Were Masking Income Risk

A meaningful portion of tenants were:

Long-term occupants

Paying far below market

Protected only by inertia, not affordability

The moment rents were pushed:

Churn risk spiked

Vacancy risk jumped

Collections became uncertain

High occupancy ≠ durable occupancy.

2. Economic Occupancy Was Lower Than It Looked

The rent roll showed:

Units occupied

Rent billed

But the effective income told a different story once normalized.

Between:

Concessions

Late or partial payments

Non-paying legacy tenants

True economic occupancy was materially lower than the physical number suggested.

This matters because:

Lenders underwrite income

Refis require collections

Cash flow requires actual dollars

3. One-Month Accounting Distorted Reality

The T-12 financials included:

Property taxes booked in a single month

Insurance booked in a single month

That made NOI appear:

Stronger in most months

“Volatile but acceptable” on average

Once normalized, the expense load was much heavier than implied.

This is a classic way deals look better than they are.

Why This Matters More in Today’s Market

In a low-rate environment, sloppy economic occupancy could be masked.

Not anymore.

Today:

Debt coverage is tighter

Refi standards are stricter

Insurance and taxes are rising

Tenant quality matters more than unit count

A deal that relies on:

Legacy tenants

Under-market rents

Deferred collections

Is not stabilized — it’s fragile.

The Underwriting Rule I Use Now

I don’t ask:

“How occupied is it?”

I ask:

What % of rents are at market?

How many tenants survive rent resets?

What happens to NOI before renovations?

What does income look like after taxes and insurance normalize?

If the deal only works once rents are fixed, collections improve, and execution is perfect — it doesn’t work.

Occupancy Is a Story. Economic Occupancy Is a System.

Deals fail when investors confuse:

Full buildings with healthy income

Stability with stagnation

Low churn with low risk

Economic occupancy tells you:

Whether the asset can survive stress

Whether debt is actually supported

Whether your exit assumptions are real

Why I Passed on This Deal

The Summer Park portfolio wasn’t “bad.”

It was just:

Overstated on stability

Underestimated on repositioning risk

Priced like a light value-add

Structured like a heavy turnaround

That mismatch is where capital gets trapped.

Final Thought

High occupancy can lie.

Economic occupancy doesn’t.

If you’re not underwriting who pays, how much they pay, and how fragile that income is, you’re guessing — not investing.

Want Help Stress-Testing Economic Occupancy?

This is exactly the kind of analysis I do for clients before they submit offers or lock up capital.

If you want:

A real underwriting teardown

Capital stack stress-testing

Exit and refi realism checks

You can see how I work here:

👉 https://chadchoquette.com/how-i-work

Or explore my deal structure services here:

👉 https://chadchoquette.com/deal-structure-services

Most deals don’t fail because they were empty.

They fail because the income wasn’t real.

If you want a second set of eyes before that happens — reach out.